NOTES TO THE FINANCIAL STATEMENTS

FOR THE YEAR ENDED DECEMBER 31, 2015

1. Description of Business

The Ottawa Macdonald-Cartier International Airport Authority (the “Authority” or “Ottawa International Airport Authority”) was incorporated January 1, 1995 as a corporation without share capital under Part II of the Canada Corporations Act and continued under the Canada Not for Profit Corporations Act on January 17, 2014. All earnings of the Authority are retained and reinvested in airport operations and development.

The objects of the Authority are:

- a) to manage, operate and develop the Ottawa International Airport, the premises of which are leased to the Authority by the Government of Canada (Transport Canada – see Note 11), and any other airport in the National Capital Region for which the Authority becomes responsible, in a safe, secure, efficient, cost effective and financially viable manner with reasonable airport user charges and equitable access to all carriers;

- b) to undertake and promote the development of the airport lands, for which it is responsible, for uses compatible with air transportation activities; and

- c) to expand transportation facilities and generate economic activity in ways which are compatible with air transportation activities.

The Authority is governed by a fourteen member Board of Directors, ten of whom are nominated by The Minister of Transport for the Government of Canada, the Government of the Province of Ontario, the City of Ottawa, the City of Gatineau, the Ottawa Chamber of Commerce, the Ottawa Tourism and Convention Authority, Chambre de commerce de Gatineau, and Invest Ottawa. The remaining four members are appointed by the Board of Directors from the community at large.

On January 31, 1997, the Authority signed a 60-year ground lease (that was later extended to 80 years in 2013) with the Government of Canada and assumed responsibility for the management, operation and development of the Ottawa International Airport.

The Authority is exempt from federal and provincial income tax, and Ontario capital tax. The Authority is domiciled in Canada. The address of the Authority’s registered office and its principal place of business is suite 2500 – 1000 Airport Parkway Private, Ottawa, Ontario, Canada, K1V 9B4.

2. Basis of Preparation and Significant Accounting Policies

The financial statements were authorized for issue by the Board of Directors on February 24, 2016.

The financial statements and amounts included in the notes to the financial statements are presented in Canadian dollars, which is the Authority’s functional currency.

The accounting policies set out below have been applied consistently to all periods presented in these financial statements.

The Authority prepares its financial statements in accordance with International Financial Reporting Standards (IFRS). These financial statements have been prepared on a historical cost basis, except, as required, for the revaluation of certain financial assets and financial liabilities to fair value.

Cash and cash equivalents

Cash and cash equivalents are defined as cash and short-term investments with original terms to maturity of 90 days or less. Such short- term investments are recorded at fair value.

Consumable supplies

Inventories of consumable supplies are valued at the lower of cost, determined on a first-in, first-out basis, and net realizable value, based on estimated replacement cost.

Property, plant and equipment

Property, plant and equipment are recorded at cost, net of government assistance, if any, and include only the amounts expended by the Authority. These assets will revert to the Government of Canada upon the expiration or termination of the Authority’s ground lease with the Government of Canada. Property, plant and equipment do not include the cost of facilities which were included in the original ground lease with the Government of Canada. Incremental borrowing costs incurred during the construction of property, plant and equipment are included in the cost.

Amounts initially recognized in respect of an item of property, plant and equipment are allocated to its significant parts and depreciated separately when the cost of the component is significant in relation to the total cost of the item and when its useful life is different from the useful life of the item. Residual values, the method of depreciation, and estimated useful lives of assets are reviewed annually and adjusted if appropriate.

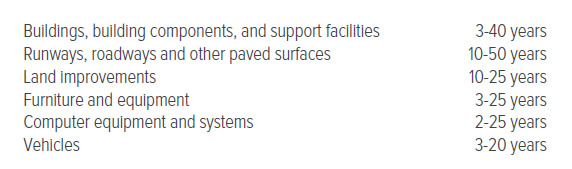

Depreciation is provided on a straight-line basis over the useful lives of individual assets and their component parts as follows:

Construction in progress is recorded at cost and is transferred to buildings and support facilities and other asset categories as appropriate when the project is complete and the asset is available for use, or is written off when, due to changed circumstances, management does not expect the project to be completed. Assets under construction are not subject to depreciation until they are available for use.

The carrying amount of an item of property, plant and equipment is derecognized on disposal or when no future economic benefits are expected from its use. The gain or loss arising from derecognition (determined as the difference between net disposal proceeds and the carrying amount of the item) is included as an adjustment of depreciation expense when the item is derecognized.

Borrowing costs

Borrowing costs are capitalized during the construction phase of qualifying assets, which are assets that take a substantial period of time to get ready for their intended use. The capitalization rate is the weighted average cost of capital of outstanding loans during the period, other than the borrowings made especially for the purpose of obtaining the asset. All other borrowing costs are recognized in interest expense on a net basis in the statement of operations and comprehensive income in the period in which they are incurred.

Impairment of non-financial assets

Property, plant and equipment and other assets are tested for impairment at the cash-generating unit level when events or changes in circumstances indicate that their carrying amount may not be recoverable, and in the case of indefinite life assets, at least annually. A cash-generating unit is the smallest group of assets that generates cash flows from continuing use that are largely independent of the cash flows of other assets or groups of assets. An impairment loss is recognized when the carrying value of the assets in the cash-generating unit exceeds the recoverable amount of the cash-generating unit.

Because the Authority’s business model is to provide services to the traveling public, none of the assets of the Authority are considered to generate cash flows that are largely independent of the other assets and liabilities of the Authority. Instead, all of the assets are considered part of the same cash-generating unit. In addition, the Authority’s unregulated ability to raise its rates and charges as required to meet its obligations, mitigates its risk of impairment losses.

Deferred financing costs

Transaction costs relating to the issuance of long-term debt, including underwriting fees, professional fees, termination of interest-rate swap agreements, and bond discounts, are deferred and amortized using the effective-interest rate method over the term of the related debt. Under the effective interest rate method, amortization is recognized over the life of the debt at a constant rate applied to the net carrying amount of the debt. Amortization is included in interest expense. Deferred financing costs are reflected as a reduction in the carrying amount of related long-term debt.

Leases

Leases or other arrangements entered into for the use of an asset are classified as either finance or operating leases.

The Authority as lessee – Except for the ground lease, the Authority typically only enters into operating leases for minor items such as photocopy machines and printers. As these leases are classified as operating leases, the payments are amortized on a straight-line basis over the lease term.

Rent imposed under the ground lease with the Government of Canada is calculated based on airport revenues for the year as defined in the lease. Accordingly, it is considered contingent rent and ground rent expense is accounted for as an operating lease in the statement of operations and comprehensive income.

The Authority as lessor – The Authority subleases land and space to other entities under operating leases. Lease income from these operating leases is recognized in income on a straight line basis over the term of the lease.

Revenue recognition

Landing fees, terminal fees, and parking revenues are recognized as the airport facilities are utilized. The Authority has a landing fee rebate incentive program which provides airlines with incentives, such as free landing fees, to operate flights to new destinations for a minimum duration of one year. These rebate obligations are recognized as a reduction of revenues until the expiry of the obligation.

Concession revenues are recognized on the accrual basis and calculated using agreed percentages of reported concessionaire sales, with specified minimum annual guarantees.

Rental revenues are recognized over the lives of respective leases, licences, and permits. Tenant inducements associated with leased premises, including the value of rent-free periods, are deferred and amortized on a straight-line basis over the term of the related lease and recognized as a reduction of rental revenues.

Airport improvement fees (“AIF”), net of airline administrative fees, are recognized upon the enplanement of passengers using information from air carriers obtained after enplanement has occurred, together with historical experience in percentages of connecting and exempt passengers. Under an agreement with the airlines, airport improvement fees are collected by the airlines in the price of a ticket and are paid to airport authorities on an estimated basis, net of airline collection fees, on the first of the month following the month of enplanement. Final settlement based on actual passenger volumes occurs at the end of the month following the month of enplanement.

Pension plan and other post-employment benefits

The Authority accrues its obligations under pension and other post- employment benefit plans as employees render the services necessary to earn these benefits. The costs of these plans are actuarially determined using the projected unit credit method based on length of service. This determination reflects management’s best estimates at the beginning of each fiscal year of the rate of salary increases, and various other factors including mortality, termination, retirement rates and expected future health care costs. For the purpose of calculating the net interest cost on the pension obligations net of pension plan assets those assets are valued at fair value.

The post-employment benefit liability recognized on the balance sheet is the present value of the defined benefit obligation at the balance sheet date less the fair value of plan assets. The accrued benefit obligation is discounted using the market interest rate on high-quality corporate debt instruments as at the measurement date, approximating the terms of the related pension liability.

Pension expense for the defined benefit pension plan includes current service cost and the net interest cost on the pension obligations net of pension plan assets calculated using the market interest rate on high-quality corporate debt instruments as determined for the previous balance sheet date. Past service costs are recognized immediately in the statement of operations. Pension expense is included in salaries and benefits on the statement of operations and comprehensive income.

Actuarial gains and losses (experience gains and losses that arise because actual experience for each year will differ from the beginning of year assumptions used for purposes of determining the cost and liabilities of these plans) are recognized in full as remeasurements of defined benefit plans in the period in which they occur, in other comprehensive income without recycling to the statement of operations and comprehensive income in subsequent periods.

Pension expense for the defined contribution pension plan is recorded as the benefits are earned by the employees covered by the plan.

Employee benefits other than post-employment benefits

The Authority recognizes the expense related to salaries, bonuses, and compensated absences such as sick leave and vacations as short-term benefits in the period the employee renders the service. Costs related to employee health, dental, and life insurance plans are recognized in the period that expenses are incurred. The liabilities related to these benefits are not discounted due to their short-term nature.

Onerous contracts

Present obligations arising under onerous contracts are recognized and measured as provisions. An onerous contract is considered to exist when the unavoidable costs of meeting the obligation under the contract exceed the economic benefits expected to be received under it.

The Authority currently has no contracts outstanding that have been designated as onerous contracts.

Estimation uncertainty and key judgments

The preparation of financial statements requires management to make estimates and assumptions that affect the reported amounts of assets, liabilities, commitments and contingencies at the date of the financial statements, and the reported amounts of revenues and expenses during the reporting period. Accounting estimates and associated assumptions are based on historical experience and other factors that are considered to be relevant. These accounting estimates and assumptions are reviewed on an ongoing basis. Actual results could significantly differ from those estimates. Adjustments, if any, will be reflected in the statement of operations in the period of settlement or in the period of revision and future periods if the revision affects both current and future periods.

Key judgment areas, estimations and assumptions include the useful lives of property, plant and equipment, valuation adjustments including allowances for uncollectible accounts, the cost of employee future benefits, and provisions for contingencies.

Collectability of trade receivables – The Authority establishes a general allowance for uncollectible accounts that involves management review of individual receivable balances based on individual customer credit worthiness, current economic trends and the condition of the industry as a whole, and analysis of historical bad debts.

Useful lives of property, plant and equipment – Critical judgments are used to determine depreciation rates, and useful lives and residual values of assets that impact depreciation amounts.

The cost of employee future benefits – The Authority accounts for pension and other post-employment benefits based on actuarial valuation information provided by the Authority’s independent actuaries. These valuations rely on statistical and other factors in order to anticipate future events. These factors include discount rates, and key actuarial assumptions such as expected salary increases, expected retirement ages, and mortality rates.

Provisions for contingencies – Provisions are recognized when the Authority has a present legal or constructive obligation as a result of past events, when it is probable that an outflow of economic resources will be required to settle the obligation, and when the amount can be reliably estimated.

Financial instruments

The Authority’s financial assets including cash and cash equivalents, accounts receivable, advances (included with prepaid expenses), and the Debt Service Reserve Fund are classified as loans and receivables. As such, they are recorded at amortized cost which approximates fair value.

The Authority’s financial liabilities including bank indebtedness, accounts payable and accrued liabilities, and long-term debt are classified as other liabilities and are accounted for at amortized cost.

Comprehensive income

Comprehensive income is defined to include net income plus or minus other comprehensive income. Other comprehensive income includes actuarial gains and losses related to the Authority’s pension plan and other post- employment benefits. In addition, other comprehensive income includes changes arising from gains and losses in the fair values of certain financial instruments and hedges, which in the Authority’s circumstances, are nil. Other comprehensive income is accumulated in a separate component of equity called accumulated other comprehensive income.

Future changes in accounting policies

IAS 17 seeks to improve the current accounting for leases by developing an approach that is more consistent with the conceptual framework definition of assets and liabilities. A lessee will be required to recognize an asset and a liability for the rights and obligations created by leases. The revised standard is applicable to fiscal periods beginning on or after January 1, 2019. The Authority is currently assessing the impact of IAS 17.

3. Sinking Fund Investments

(tabular amounts in thousands of dollars)

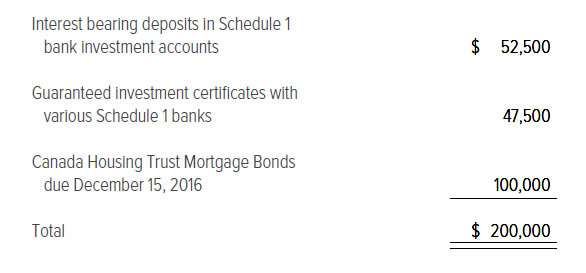

On June 9, 2015, the Authority completed the issuance of $300.0 million of Series E Amortizing Revenue Bonds (see Note 8). Of the net proceeds from this issuance, $200.0 million was placed in a segregated fund maintained by the Trustee and has been invested in accordance with the Board-approved Investment Policy. These investments will be used to retire the Authority’s Series D Revenue Bonds maturing on May 2, 2017.

As at December 31, 2015 Sinking Fund investments consist of the following:

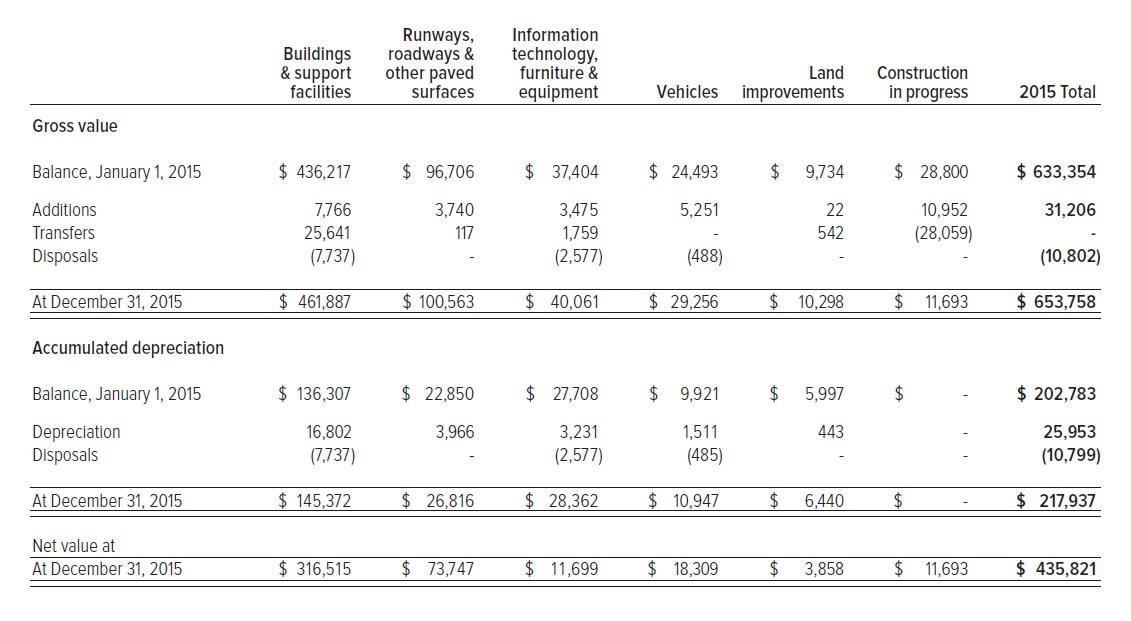

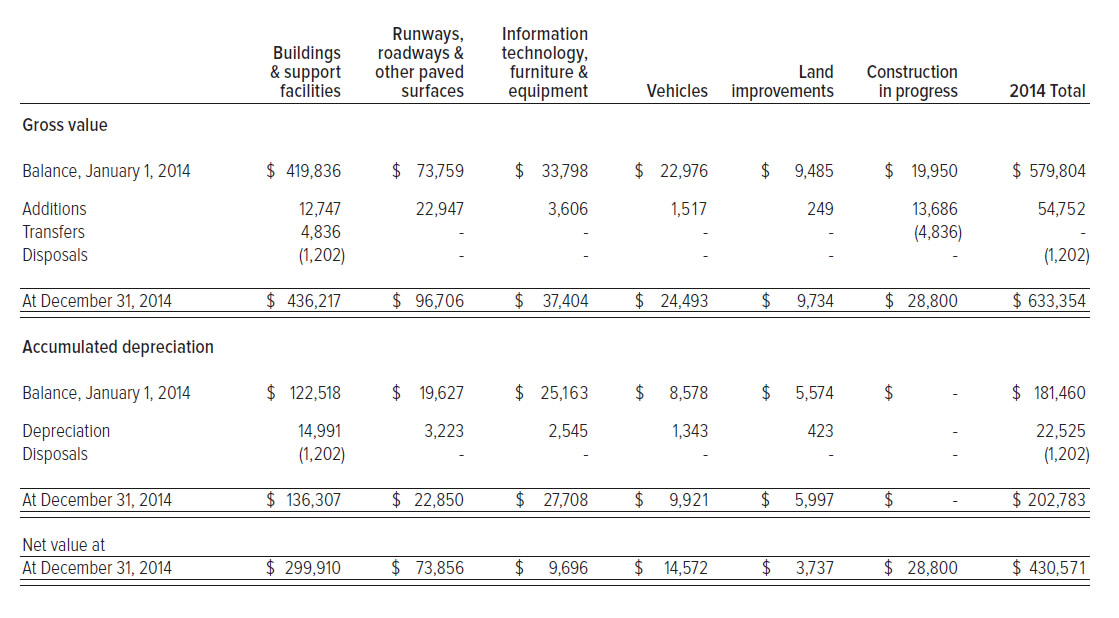

4. Property, Plant and Equipment

(tabular amounts in thousands of dollars)

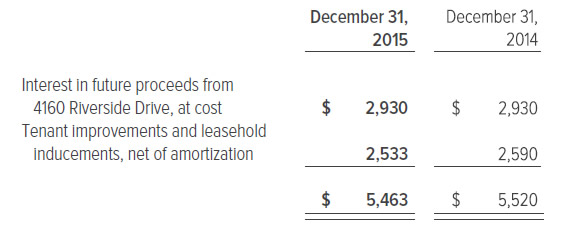

5. Other Assets

(tabular amounts in thousands of dollars)

Interest in future proceeds from 4160 Riverside Drive

In an agreement signed on May 27, 1999, the Authority agreed to assist the Regional Municipality of Ottawa-Carleton (now the City of Ottawa) in acquiring lands municipally known as 4160 Riverside Drive by contributing to the City of Ottawa 50.0% of the funds required for the acquisition. In return, the City agreed to place restrictions on the use of the lands to ensure the lands are used for purposes that are compatible with the operations of the Authority. In addition, the Authority will receive 50% of the net proceeds from any future sale, transfer, lease, or other conveyance of the lands.

Tenant improvements and leasehold inducements

During 2011, the Authority entered into a long-term lease with a subtenant that included a 3-year rent-free period and provided, as a tenant inducement, a payment in the amount of $1.5 million towards the cost of utilities infrastructure and other site improvements. Tenant inducements associated with leased premises, including the value of rent free periods, are deferred and amortized on a straight-line basis over the term of the related lease and recognized as a reduction of rental revenues. The value of these tenant inducements is being recognized as a reduction in rent during the first 20 years of the 47 year term of the lease.

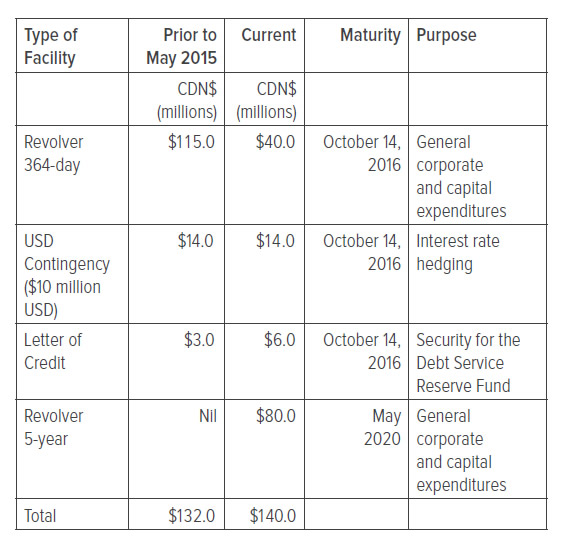

6. Credit Facilities

The Authority maintains access to an aggregate of $140.0 million ($132.0 million prior to May 2015) in committed Credit Facilities with two Canadian banks. In May 2015, some of the Credit Facilities were renegotiated in advance of the Series E bond financing. Facilities were increased to better reflect current financial requirements of the Authority. The 364-day facilities that expired on October 17, 2015 have been extended for another 364-day term expiring on October 14, 2016. These facilities are secured under the Master Trust Indenture (see Note 8) and are available by way of overdraft, Prime Rate Loans, or Bankers’ Acceptances. Indebtedness under these facilities bears interest at rates that vary with the lender’s prime rate and Bankers’ Acceptance rates, as appropriate.

The following table summarizes the amounts available under each of these Credit Facilities, along with their related expiry dates and intended purposes:

As at December 31, 2015, $13.2 million of these revolving facilities had been designated to the Operating and Maintenance Reserve Fund (see Note 8).

In order to satisfy the Debt Service Reserve Fund requirement for the Series E Bonds, $5.9 million of the Authority’s Credit Facility has been designated to an irrevocable standby letter of credit in favour of the Trustee.

As at December 31, 2014, the bank indebtedness under these facilities incurred interest at an average rate of 1.77%.

7. Capital Management

The Authority is incorporated without share capital under the Canada Not for Profit Corporations Act and, as such, all earnings are retained and reinvested in airport operations and development. Accordingly, the Authority’s only sources of capital for investing in airport operations and development are bank debt, long-term debt and accumulated earnings included on the Authority’s balance sheet as Retained Earnings.

The Authority incurs debt, including bank debt and long-term debt, to finance development. It does so on the basis of the amount that it considers that it can afford and manage based on revenues from airport improvement fees (AIF) and to maintain a minimum AIF: debt service coverage ratio. This provides for a self-imposed limit on what the Authority can spend on major development of the airport, such as the Authority’s major infrastructure construction programs.

The Authority manages its rates and charges for aeronautical and other fees to safeguard the Authority’s ability to continue as a going concern and to maintain a conservative capital structure. It makes adjustments to these rates in light of changes in economic conditions and events, and to maintain sufficient net earnings to meet ongoing debt coverage requirements.

The Authority is not subject to capital requirements imposed by a regulator, but manages its capital to comply with the covenants of its Master Trust Indenture (see Note 8(a)) and to maintain its credit ratings in order to secure access to financing at a reasonable cost.

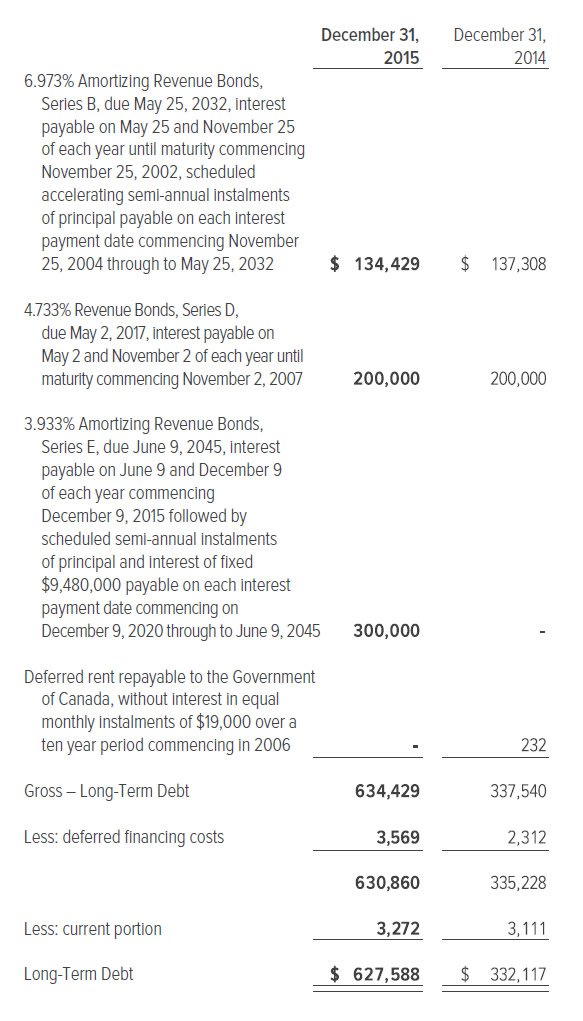

8. Long-Term Debt

(tabular amounts in thousands of dollars)

a) Bond Issues

In May 2002, the Authority completed its original $270.0 million Revenue Bond issue with two series, the $120.0 million Revenue Bonds, Series A at 5.64% due on May 25, 2007 and the $150.0 million Amortizing Revenue Bonds, Series B at 6.973% due on May 25, 2032. In May 2007, the Authority completed a $200.0 million Revenue Bond issue, in part to refinance the Series A, Revenue Bonds repaid on May 25, 2007. The $200.0 million Revenue Bonds, Series D at 4.733% are due on May 2, 2017 and Sinking Funds have been set aside as at December 31, 2015 to extinguish the outstanding amount (see Series E below).

On June 9, 2015 the Authority completed a $300.0 million Amortizing Revenue Bond issue which bears interest at a rate of 3.933% due on June 9, 2045. Part of the net proceeds from this offering were used to pre-fund the repayment of the Series D Bonds by depositing $200.0 million into a segregated fund held by the Trustee (see Note 3). Prior to the closing of the offering, a bond forward transaction was entered into to protect from volatility in interest rates and it resulted in a $1.6 million gain being recorded. The Authority has elected not to apply hedge accounting with respect to this forward transaction, therefore the related gain has been recognized in the statement of operations and comprehensive income for the year.

The Bonds are redeemable, in whole or in part, at the option of the Authority at any time, or in the case of the Series E Bonds, until six months prior to the maturity date, upon payment of the greater of (i) the aggregate principal amount remaining unpaid on the Bonds to be redeemed, and (ii) the value which would result in a yield to maturity equivalent to that of a Government of Canada bond of equivalent maturity plus a premium. The premium is 0.24% for the Series B Bonds, 0.14% for the Series D Bonds and 0.42% for the Series E Bonds. If the Series E Bonds are redeemed within six months of the maturity date, the Series E Bonds will be redeemable at a price equal to 100.0% of the principal amount outstanding plus any accrued and unpaid interest.

The net proceeds from these offerings were used to finance the Authority’s infrastructure construction programs, and for general corporate purposes. These purposes included refinancing existing bank indebtedness incurred by the Authority in connection with these construction programs and funding of the Debt Service Reserve Fund.

Under the Master Trust Indenture entered into by the Authority in connection with the original debt offering in May 2002, all of these bond issues are direct obligations of the Authority ranking pari passu with all other indebtedness issued. All indebtedness, including indebtedness under bank credit facilities, are secured under the Master Trust Indenture by an assignment of revenues and related book debts, a security interest on money in reserve funds and certain accounts of the Authority, a security interest in leases, concessions and other revenue contracts of the Authority, and an unregistered mortgage of the Authority’s leasehold interest in airport lands.

The Authority is unregulated in its ability to raise its rates and charges as required to meet its obligations. Under the Master Trust Indenture, the Authority is required to take action, such as increasing its rates, should its projected debt service coverage ratio fall below 1.0. If this debt service covenant is not met in any year, the Authority is not in default of its obligations under the Master Trust Indenture as long as the test is met in the subsequent year.

Pursuant to the terms of the Master Trust Indenture, the Authority is required to maintain with the Trustee, a Debt Service Reserve Fund equal to six months’ debt service in the form of cash, qualified investments or letter of credit. At December 31, 2015, the balance of cash and qualified investments held in the Debt Service Reserve Fund was $11.2 million. Furthermore, in order to satisfy the Debt Service Reserve Fund requirement for the Series E Bonds, $5.9 million of the Authority’s Credit Facilities has been designated to an irrevocable standby letter of credit in favour of the Trustee. These trust funds are held for the benefit of the bondholders for use and application in accordance with the terms of the Master Trust Indenture. In addition, the Authority is required to maintain an Operating and Maintenance Reserve Fund equal to 25.0% of defined operating and maintenance expenses in the previous year (approximately $13.2 million in 2015 based on 2014 expenses). The Operating and Maintenance Reserve Fund has been satisfied by the undrawn availability under the committed credit facility (see Note 6).

At December 31, 2015 the Authority was in full compliance with the provisions of its debt facilities, including the Master Trust Indenture’s provisions related to reserve funds, the flow of funds and the rate covenant.

(b) On July 16, 2003, the Minister of Transport announced short-term rent relief for airports. Under this program, the Authority was able to defer approximately 10.0% of its rent for the two-year period that started July 1, 2003 (a total of $2.3 million). The deferral is to be repaid, interest-free, over a period of 10 years that started on January 1, 2006 and ended on December 31, 2015. Because this is a deferral and not a permanent reduction of rent, the full amounts of rent were recorded as a liability in the accounts.

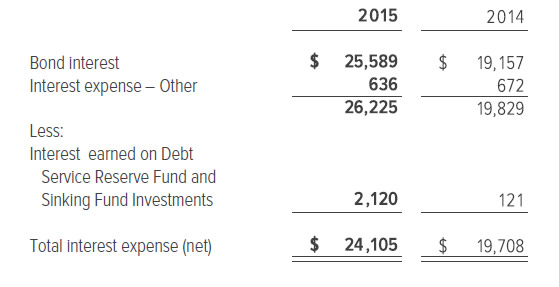

c) Interest expense (net)

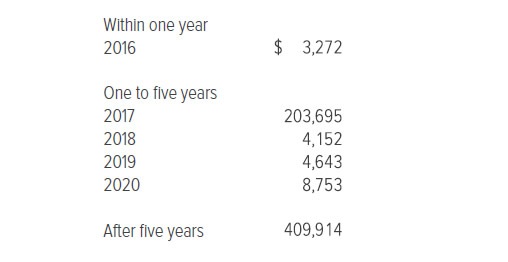

d) The future annual principal payments for all long-term debt are as follows:

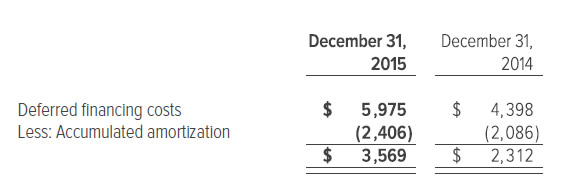

e) Deferred financing costs

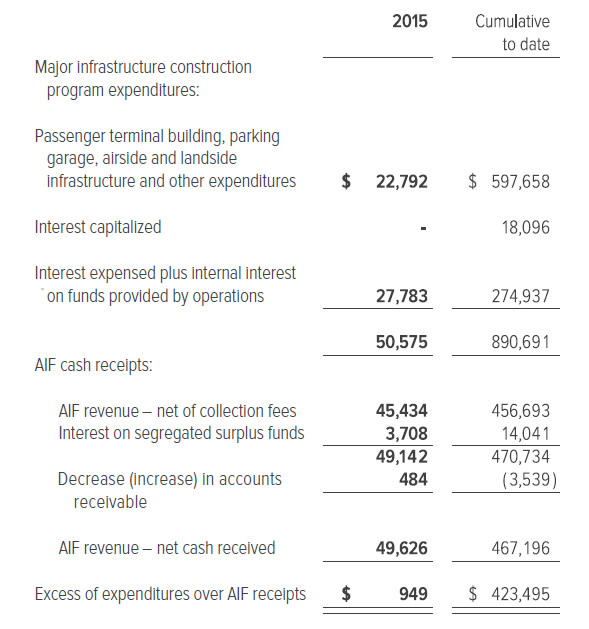

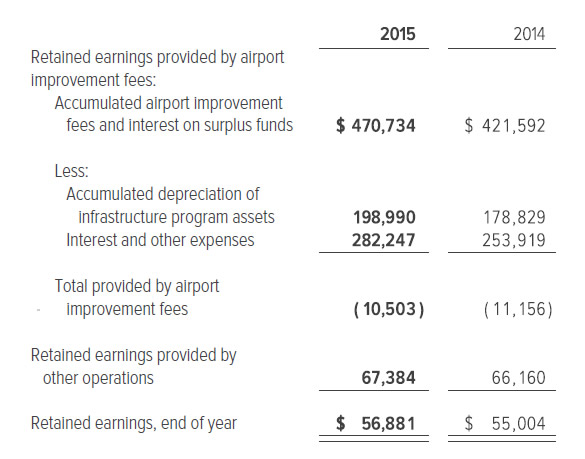

9. Airport Improvement Fees (AIF)

(tabular amounts in thousands of dollars)

Airport improvement fees are collected by air carriers under an agreement between the Authority, the Air Transport Association of Canada, and the air carriers serving the airport. Under the agreement, AIF revenues may only be used to pay for the capital and related financing costs of major airport infrastructure development. AIF revenues are recorded net of collection fees of 6.0% withheld by air carriers of $2.9 million (2014 - $2.8 million).

The AIF will continue to be collected until the cumulative excess of expenditures over AIF receipts is reduced to zero.

Retained earnings of the Authority as at December 31 are as follows:

10. Pension Plan and Other Post-Employment Benefits

(tabular amounts in thousands of dollars)

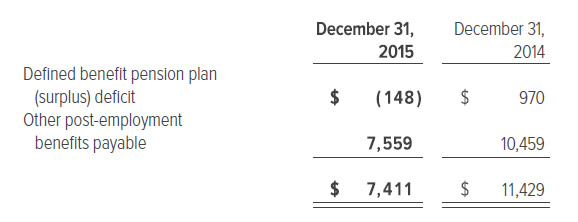

The post-employment benefit liability included in the balance sheet as a long-term liability is as follows:

The Authority sponsors and funds a pension plan for its employees, which has defined benefit and defined contribution components.

Under the defined contribution plan, the Authority pays fixed contributions into an independent entity to match certain employee contributions. The Authority has no legal or constructive obligation to pay further contributions after its payment of the fixed contribution.

The defined benefit plan includes employees who were employees of the Authority on the date of transfer of the responsibility for the management, operation and development of the Ottawa Macdonald-Cartier International Airport from Transport Canada on January 31, 1997 (see Note 1), including former Transport Canada employees, the majority of whom transferred their vested benefits from the Public Service Superannuation Plan to the Authority’s pension plan. Pension benefits payable under the defined benefit component of the plan are based on members’ years of service and the average of the best six years’ consecutive earnings near retirement up to the maximums allowed by law. Benefits are indexed annually to reflect the increase in the consumer price index to a maximum of 8.0% in any one year.

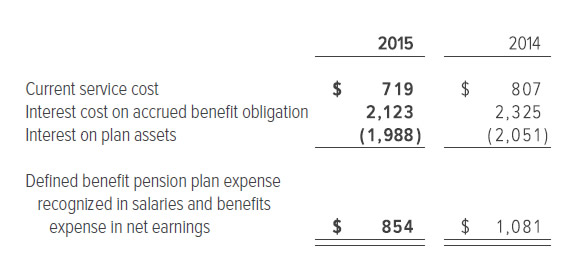

Pension plan costs are charged to operations as services are rendered based on an actuarial valuation of the obligation.

In addition to pension plan benefits, the Authority provides other post-employment and retirement benefits to its employees including health care insurance and lump sum payments upon retirement or termination of employment. The Authority accrues the cost of these future benefits as employees render their services based on an actuarial valuation. This plan is not funded.

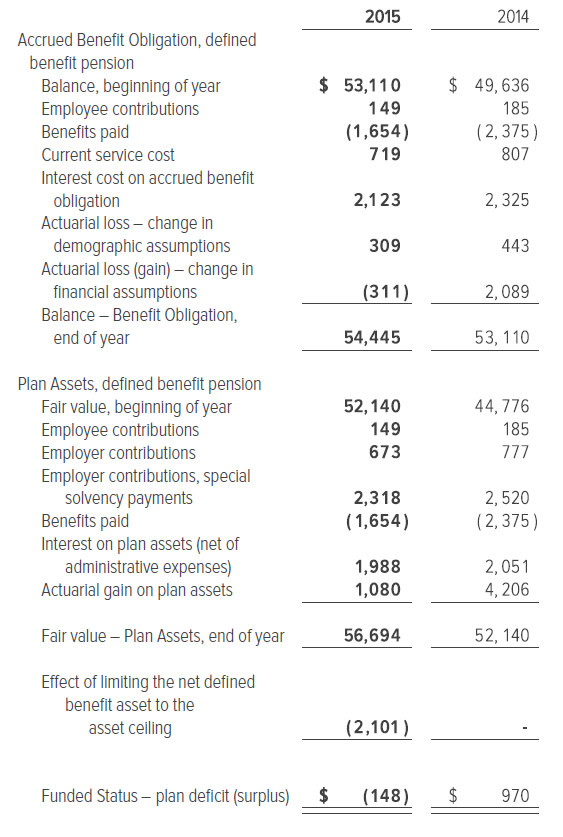

As at the date of the most recent actuarial valuation of the pension plan which was as at December 31, 2014 that was completed and was filed in June 2015 as required by law, the plan had a deficit on a funding (going concern) basis of $1,761,000 assuming a discount rate of 4.25% ($4,258,800 as at December 31, 2013 assuming a discount rate of 5.00%). This amount differs from the amount reflected below primarily because the obligation is calculated using the discount rate that represents the expected long-term rate of return of assets. For accounting purposes, it is calculated using an interest rate determined with reference to market rates on high-quality debt instruments with cash flows that match the timing and amount of expected benefit payments.

The Pension Benefits Standards Act, 1985 requires that a solvency analysis of the plan be performed to determine the financial position (on a “solvency basis”) of the plan as if it were fully terminated on the valuation date due to insolvency of the sponsor or a decision to terminate. At December 31, 2014, the plan had a deficit on a solvency basis of $11,591,500 ($11,520,800 as at December 31, 2013) before considering the present value of additional solvency payments required under the Act. In 2015, the Authority made additional solvency payments of $2,318,300 ($2,520,000 in 2014) to amortize this deficiency.

The next required actuarial valuation of the defined benefit pension plan, which will be as at December 31, 2015, is scheduled to be completed and filed by its June 2016 due date. The plan’s funded position and the amounts of solvency payments required under The Pension Benefits Standards Act, 1985 are subject to fluctuations in interest rates. It is expected that, once the actuarial valuation is completed, the additional solvency payments that will be required for 2016 will be approximately $2,318,000 (2015 - $2,318,300). In addition, the Authority expects to contribute approximately $673,000 (2015 - $642,000) on account of current service in 2016 to the defined benefit component of the pension plan for the year ending December 31, 2016.

Based on the most recent actuarial determination of pension plan benefits completed as at December 31, 2014 and extrapolated to December 31, 2015 by the Authority’s actuaries, the estimated status of the defined benefit pension plan is as follows:

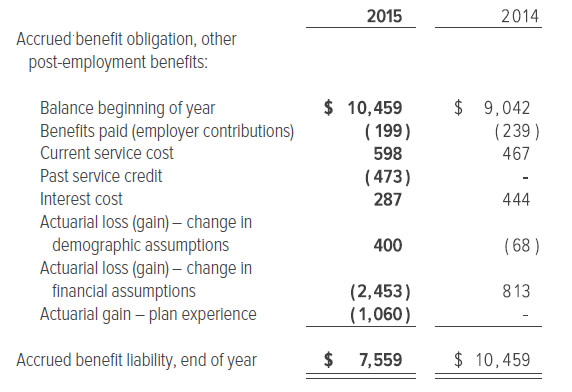

In addition to pension benefits, the Authority provides other post-employment benefits to its employees. The status of other post-employment benefit plans as at December 31 is as follows:

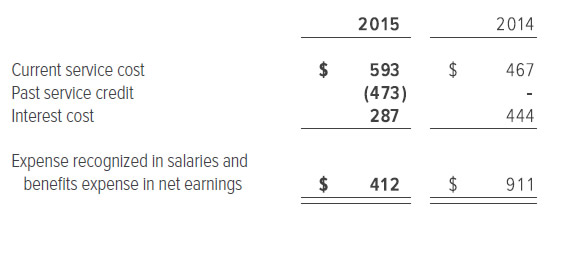

The net expense for other post-employment benefit plans for the year ended December 31 is as follows:

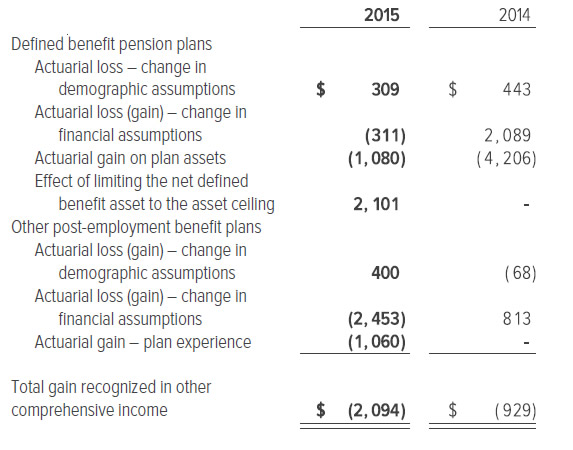

The amount recognized in other comprehensive income for pension plans and other post-employment benefit plans for the year ended December 31 is as follows:

The costs of the defined benefit component of the pension plan and of other post- employment benefits are actuarially determined using the projected benefit method prorated on services. This determination reflects management’s best estimates of the rate of return on plan assets, rate of salary increases, and various other factors including mortality, termination, and retirement rates.

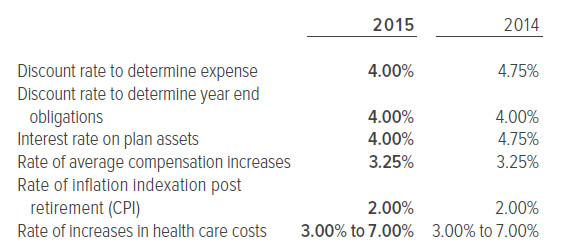

The significant economic assumptions used by the Authority’s actuaries in measuring the Authority’s accrued benefit obligations as at December 31 are as follows:

The Authority’s defined benefit pension plans and post-retirement benefit plans face a number of risks, including inflation, but the most significant of these risks relates to changes in interest rates (discount rate). The defined benefit pension plan’s liability is calculated for various purposes using discount rates set with reference to corporate bond yields. If plan assets underperform this yield, this will increase the deficit. A decrease in this discount rate will increase plan liabilities, although this will be partially offset by an increase in the value of the plan’s bond holdings. Relative to the actuarial assumptions used in the valuation of the pension plan obligations, a 1.0% increase in the discount rate will decrease the obligation by $7.4 million. A 1.0% decrease in the discount rate will increase the obligation by $9.4 million. Based on calculations by the Authority’s actuaries included in the actuarial valuation as at December 31, 2014, the impact of a 1.0% decrease in discount rate will increase the solvency liability by $12.6 million.

In addition to the risks of fluctuations in interest rates (discount rate) outlined above, the Authority’s pension plans are subject to a number of other risks. Relative to the assumptions noted above, it is estimated that a 1.0% increase in the rate of inflation, will increase the defined benefit obligation by $8.4 million. A decrease of 1.0% will decrease the obligation by $6.8 million. It is estimated that a 1.0% increase in the compensation assumption will increase the defined benefit obligation by $0.6 million. It is estimated that a one year increase in life expectancy will increase the defined benefit obligation by $1.3 million and increase the obligation for other post-employment benefits by $0.2 million. A 1.0% decrease in the discount rate would increase the estimated obligation for post-employment benefits by approximately $1.1 million and a 1.0% increase in the discount rate would decrease the obligation by $0.8 million. A 1.0% increase in health care costs would increase the obligation for post-employment benefits by an estimated $1.1 million.

The Authority’s pension and post-employment benefit plans are designed to provide benefits for the life of the member. Increases in life expectancy will result in an increase in the plans’ liabilities. This is particularly significant because inflation increases result in higher sensitivity to changes in life expectancy. The obligations for these plans as at December 31, 2015 have been estimated by the Authority’s actuaries using the most recent mortality tables available (Canadian Pensioner Mortality 2014 Combined Sector Mortality Table).

The investment policy for the pension plan’s defined benefit funds was revised in early 2012 to adopt a “glide-path” de-risking strategy to better match fluctuations in the accrued benefit obligation due to changes in interest rates. Under this strategy, the proportion of liability matching assets (fixed income funds) will be increased and the proportion of growth assets (equity and other funds) will be decreased over time as the average age of active members increases and as the plan’s solvency ratio improves. The plan’s solvency ratio is monitored monthly by the plan’s actuaries. The defined benefit plan is a closed plan. As at the date of the most recent actuarial valuation at December 31, 2014, the average age of the 27 active members was 53 years of age. The average age of the 54 retired members was 66 years of age.

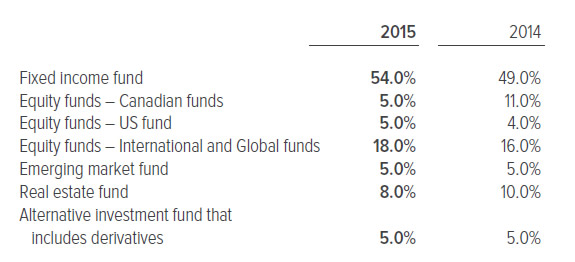

Responsibility for governance of the plans including overseeing aspects of the plans such as investment decisions lies with the Authority through a Pension Committee. The Pension Committee in turn has appointed experienced independent experts such as investment advisors, investment managers, actuaries and a custodian for assets. In accordance with the investment policy for the pension plan’s defined benefit funds, as at December 31 the plan’s non-current, non-cash assets are invested in funds maintained by Manulife (formerly Standard Life Assurance Company of Canada) and managed by various investment managers as follows:

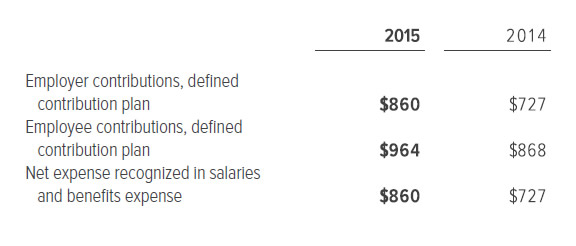

The Authority’s contribution to the defined contribution component of the pension plan is a maximum of 8% of the employee’s gross earnings to match employee contributions. Information on this component is as follows:

11. Financial Instruments

(tabular amounts in thousands of dollars)

Fair values

None of the Authority’s financial assets or liabilities are reflected in the financial statements at fair values (see Note 2).

The Authority’s long-term debt, including Revenue bonds outstanding, is reflected in the financial statements at amortized cost. As at December 31, 2015, the estimated fair value of the long-term Series B, Series D and Series E Revenue Bonds was $179.2 million, $210.8 million and $297.5 million, respectively (2014 - $178.7 million and $215.5 million for Series B and Series D Revenue Bonds, respectively). The fair value of the bonds is estimated by calculating the present value of future cash flows based on year-end benchmark interest rates and credit spreads for similar instruments.

Risk Management

The Authority is exposed to a number of risks as a result of the financial instruments on its balance sheet that can affect its operating performance. These risks include interest rate risk, liquidity risk, credit risk, and concentration risk. The Authority’s financial instruments are not subject to foreign exchange risk or other price risk.

Interest rate risk

Interest rate risk is the risk that the fair value or future cash flows of a financial instrument will fluctuate because of changes in market interest rates.

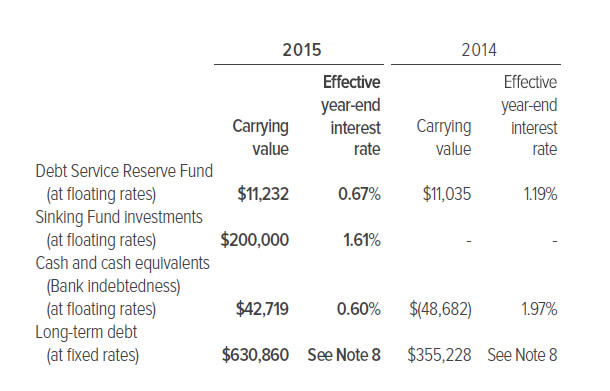

The following financial instruments are subject to interest rate risk as at December 31:

The Authority has entered into fixed rate long-term debt, and accordingly, the impact of interest rate fluctuations has no effect on interest payments until such time as this debt is to be refinanced. Changes in prevailing benchmark interest rates and credit spreads, however, may impact the fair value of this debt. The Authority’s most significant exposure to interest-rate risk relates to its future anticipated borrowings and refinancing, which are not expected to occur in the near-term.

In addition, the Authority’s bank indebtedness, cash and cash equivalents, and its Debt Service Reserve Fund are subject to floating interest rates. Management has oversight over interest rates that apply to its cash and cash equivalents, and its debt service reserve fund. These funds are invested from time to time in short-term bankers’ acceptances permitted by the Master Trust Indenture, while maintaining liquidity for purposes of investing in the Authority’s capital programs. Management has oversight over interest rates that apply to its bank indebtedness and fixes these rates for short term periods of up to 90 days based on bankers’ acceptance rates.

If interest rates had been 50 basis points (0.50%) higher/lower and all other variables were held constant, including timing of expenditures related to the Authority’s capital expenditure programs, the Authority’s earnings for the year would have increased/decreased by $0.5 million as a result of the Authority’s exposure to interest rates on its floating rate assets and liabilities. Management believes, however, that this exposure is not representative of the exposure during the year, and that interest income is not essential to the Authority’s operations as these assets are intended for reinvestment in airport operations and development, and not for purposes of generating interest income.

Liquidity risk

The Authority manages its liquidity risks by maintaining adequate cash and credit facilities, by updating and reviewing multi-year cash flow projections on a regular and as-needed basis, and by matching its long-term financing arrangements with its cash flow needs. In view of its excellent credit ratings, the Authority has ready access to sufficient long-term funds as well as committed lines of credit through credit facilities with two Canadian banks.

The Authority is unregulated in its ability to raise its rates and charges as required to meet its obligations. Under the Master Trust Indenture entered into by the Authority in connection with its debt offerings (see Note 8), the Authority is required to take action, such as increasing its rates, should its projected debt service coverage ratio fall below 1.0. If this debt service covenant is not met in any year, the Authority is not in default of its obligations under the Master Trust Indenture as long as the test is met in the subsequent year. Because of the Authority’s unfettered ability to increase rates and charges it expects to continue to have sufficient liquidity to cover all of its obligations as they come due, including interest payments of approximately $20.0 million per year. The future annual principal payment requirements of the Authority’s obligations under its long-term debt are described in Note 8(e).

Credit and concentration risks

The Authority is subject to credit risk through its cash and cash equivalents, its Debt Service Reserve Fund, and its trade and other receivables. The counterparties of cash, cash equivalents and the Debt Service Reserve Fund are highly rated Canadian financial institutions. The trade and other receivables consist primarily of current aeronautical fees and airport improvement fees owing from air carriers. The majority of the Authority’s accounts receivable are paid within 35 days of the date that they are due. A significant portion of the Authority’s revenues, and resulting receivable balances, are derived from air carriers. The Authority performs ongoing credit valuations of receivable balances and maintains an allowance for potential credit losses. The Authority’s right under the Airport Transfer (Miscellaneous Matters) Act to seize and detain aircraft until outstanding aeronautical fees are paid mitigates the risk of credit losses.

The Authority derives approximately 50.0% (47.0% in 2014) of its landing fee and terminal fee revenue from Air Canada and its affiliates. Management believes, however, that the Authority’s long-term exposure to any single airline is mitigated by the fact that approximately 93.0% (92.0% in 2014) of the passenger traffic through the airport is origin and destination traffic, and therefore other carriers are likely to absorb the traffic of any carrier that ceases operations. In addition, the Authority’s unfettered ability to increase its rates and charges mitigates the impact of these risks.

12. Operating Leases

The Authority as lessee: On January 31, 1997, the Authority signed a 60-year ground lease with the Government of Canada (Transport Canada) for the management, operation and development of Ottawa International Airport. The ground lease contains provisions for compliance with a number of requirements, including environmental standards, minimum insurance coverage, specific accounting and reporting requirements, and various other matters that have a significant effect on the day-to-day operation of the airport. The Authority believes that it has complied with all requirements under the ground lease.

On February 25, 2013, the Minister of Transport for the Government of Canada signed an amendment to the ground lease to extend the lease term from 60 years to 80 years, ending on January 31, 2077. At the end of the renewal term, unless otherwise extended, the Authority is obligated to return control of the airport to the Government of Canada.

In 2005, the Government of Canada announced the adoption of a new rent policy that has resulted in reduced rent for Canadian airport authorities, including Ottawa Macdonald-Cartier International Airport Authority. Under this formula, rent is calculated as a royalty based on a percentage of gross annual revenues on a progressive scale.

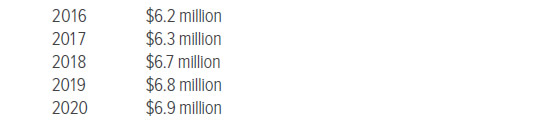

Based on forecasts of future revenues (which are subject to change depending on economic conditions and changes in the Authority’s rates and fees), estimated ground rent payments for the next five years are approximately as follows:

The Authority as lessor: The Authority leases out, under operating leases, land and certain assets that are included in property, plant and equipment. Many leases include renewal options, in which case they are subject to market price revision. The lessee does not have the possibility of acquiring the leased assets at the end of the lease.

The estimated lease revenue for the next five years is approximately as follows:

13. Changes in Non-Cash Working Capital Related To Operations

(in thousands of dollars)

14. Related Party Transactions

(tabular amounts in thousands of dollars)

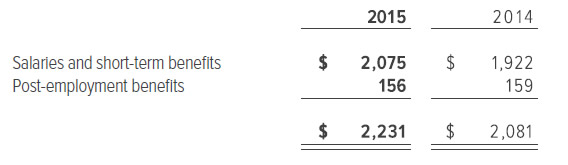

Compensation paid, payable, or provided by the Authority to key management personnel during the year ended December 31 was as follows:

Key management includes the Authority’s Board of Directors and members of the Executive team, including the President and CEO, and six Vice-Presidents.

The defined pension plan referred to in Note 10 is a related party to the Authority. The Authority’s transactions with the pension plan include contributions paid to the plan, which are disclosed in Note 10. The Authority has not entered into other transactions with the pension plan and has no outstanding balances with the pension plan at the balance sheet date.

15. Commitments and Contingencies

Ground Lease Commitments

The operating lease for the Airport requires the Authority to calculate rent payable to Transport Canada utilizing a formula reflecting annual airport revenues (see Note 12).

Operating Commitments

The Authority has operating commitments in the ordinary course of business requiring payments of $8.4 million in 2015 and diminishing in each year over the next 5 years as contracts expire. At December 31, 2015, the total of these operating commitments amounted to $10.7 million. These commitments are in addition to contracts for the purchase of property, plant, and equipment of approximately $11.0 million.

Contingencies

The Authority may, from time to time, be involved in legal proceedings, claims and litigation that arise in the ordinary course of business. The Authority does not expect the outcome of any proceedings to have a material adverse effect on the financial position or results of operations of the Authority.

16. Post-Reporting Date Events

No adjusting or significant non-adjusting events have occurred between the reporting date and February 24, 2016 when the financial statements were authorized for issue.