2014 FINANCIAL REVIEW

This Financial Review reports on the results and financial position of the Ottawa International Airport Authority (the Authority) for its year ended December 31, 2014.

This review should be read in conjunction with the audited financial statements and related notes of the Authority. This review contains forward–looking statements, including statements regarding the business and anticipated financial performance of the Authority. These statements are subject to a number of risks and uncertainties that will cause actual results to differ from those contemplated in the forward–looking statements.

OVERALL PERFORMANCE

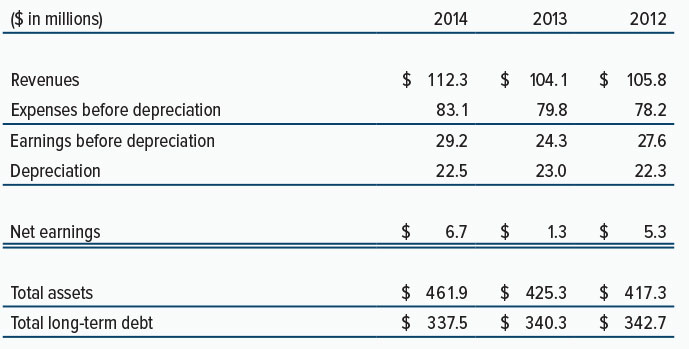

Earnings before depreciation for the year ended December 31, 2014 were $29.2 million compared to $24.3 million for the year ended December 31, 2013. An increase in the airport improvement fee from $20 per enplaned passenger to $23 per enplaned passenger effective March 1, 2014 was the most significant factor impacting earnings for the year.

The Authority recorded depreciation of $22.5 million in 2014 compared to $23.0 million in 2013, reflecting depreciation of the terminal building and related facilities over their estimated economic lives. After subtracting depreciation, the Authority generated net earnings of $6.7 million in 2014 compared to $1.3 million in 2013.

The Authority’s net operating results for the three years ended December 31, 2014 are summarized as follows:

RESULTS OF OPERATIONS

OPERATING ACTIVITIES

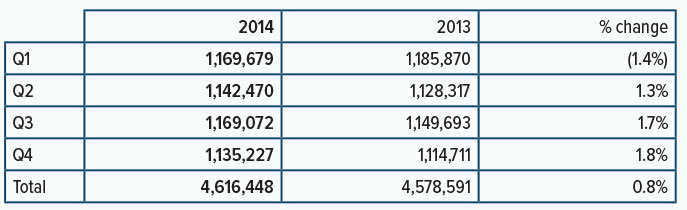

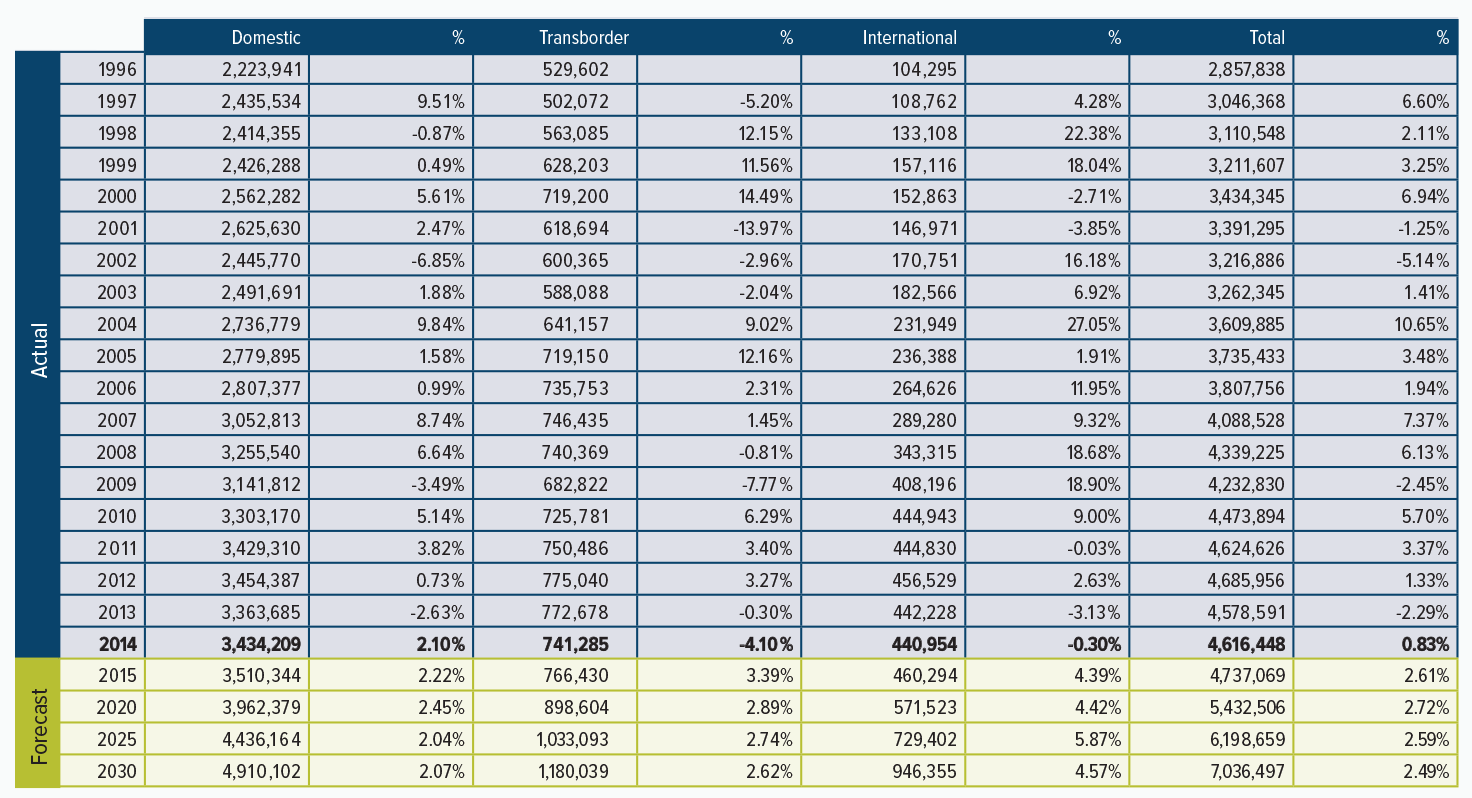

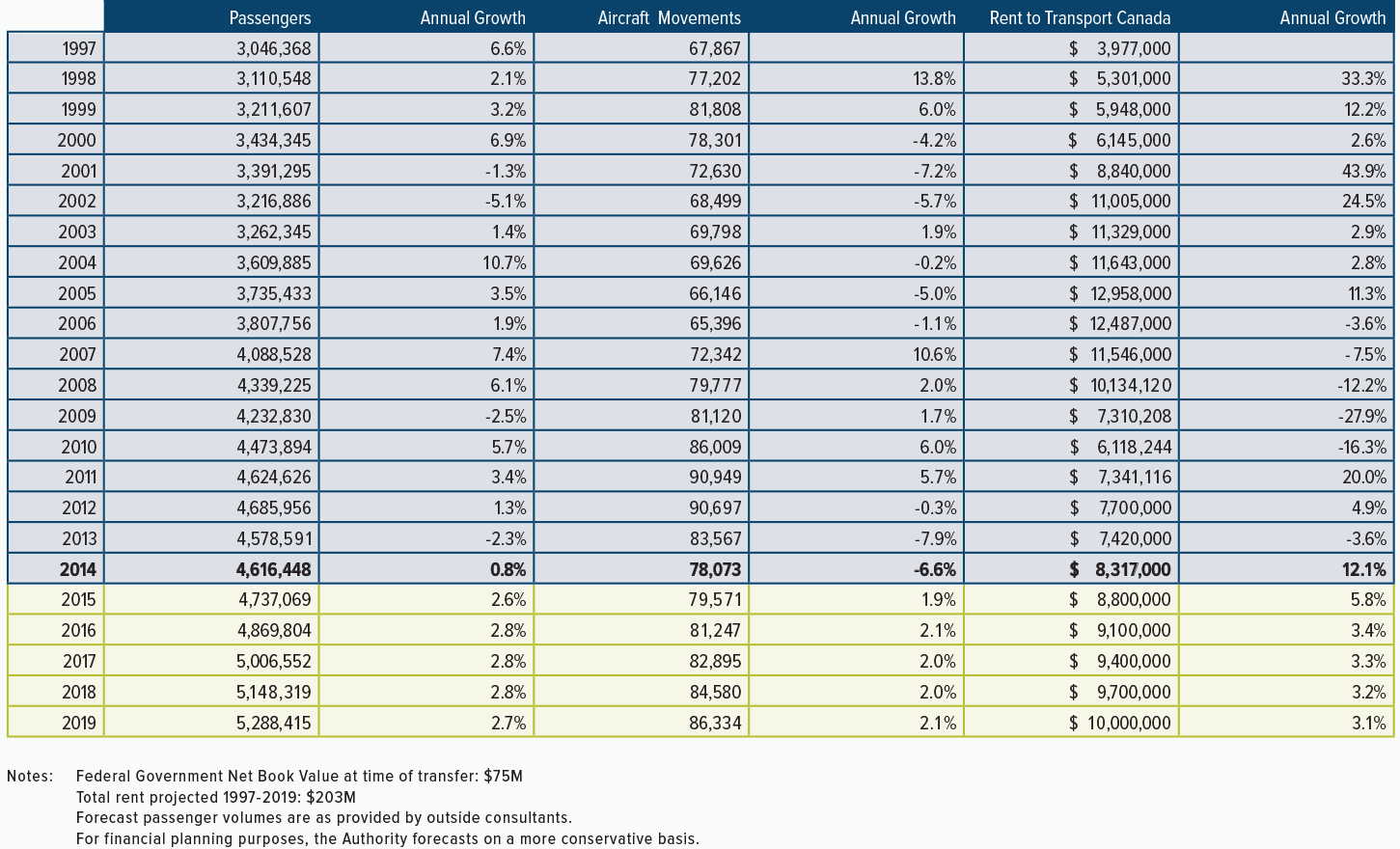

During 2014, the Ottawa Airport saw passenger volumes increase by 0.8% from 2013 volumes. A slowdown in passenger volumes had started in May 2012, when previously strong year-over-year growth in monthly volumes flattened and, by September 2012, growth turned negative. Volumes remained somewhat depressed until the second half of 2014 when passenger traffic started to track just slightly ahead of volumes seen in 2013 and also ahead of 2011, before the decline started. A total of 4,616,448 enplaned and deplaned passengers moved through the airport in 2014 as compared to 4,578,591 passengers in 2013.

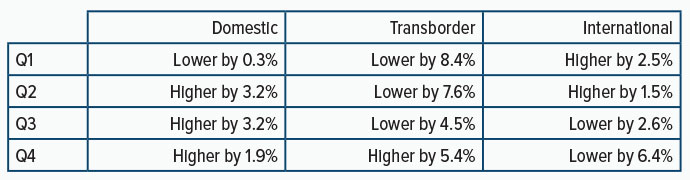

Passenger volumes between Ottawa and domestic locations were 2.1% higher in 2014 than in 2013. All domestic carriers saw domestic volumes increase in 2014. The slowdown in growth that started in May 2012 had been most noticeable in domestic volumes. Passenger volumes between Ottawa and domestic locations saw some growth from 2013 in the second, third, and fourth quarters after remaining flat from 2013 in the first quarter. Economic conditions in Canada have improved. Local conditions in Ottawa, where the threat of government job cuts and other government cost cutting impacted travel plans, have improved as well, although not as strongly as in the rest of Canada. Due to transborder capacity constraints (2014 transborder seat volumes were 7.3% less than in 2013), some U.S. bound passengers may now be reaching their destinations by other means, including connections through Toronto.

Porter’s promotional pricing strategy continued to stimulate demand, especially during off-peak times, with other airlines competing to match this pricing. This demand returned in 2014 with Porter showing the greatest percentage increase in passengers among domestic carriers. Service to Toronto Billy Bishop Airport continued to be a popular option for accessing Toronto, particularly for business travellers, but also for leisure travellers taking advantage of off-peak promotional pricing.

Transborder volumes were 4.1% lower than in 2013. Passenger volumes have been impacted by transborder capacity cuts by U.S. carriers (American Airlines eliminated its service to Ottawa). In addition, since the second quarter of 2013 when charter carriers began to plan their packages, and leisure travellers began to book their winter vacations for the 2013/2014 season, the Canadian dollar has decreased in value against the U.S. dollar. Discretionary leisure travel decisions have been impacted by this weakness in the Canadian dollar.

International volumes decreased by 0.3% in 2014. Increased activity occurred primarily in the first half of 2014 during winter charter season, but the third and fourth quarter volumes were lower than in 2013. Air Canada temporarily eliminated its direct flight to Frankfurt during the second half of the year, providing explanation for a portion of this decrease.

By sector, each quarter of 2014 passenger volumes compared to comparable quarters in 2013 were as follows:

By quarter, total passenger volumes were as follows:

The size (weight) of an aircraft and number of “landed” seats on an aircraft (regardless of whether those seats are occupied by passengers) are the most significant factors in the determination of aeronautical fees charged to airlines. In 2014, the number of landed seats decreased by 0.8% from 2013. The largest decreases in seats came during the first quarter, primarily due to flight cancellations due to worse than normal winter weather conditions in the first quarter of 2014. The total year decrease was most pronounced in landed seats to transborder and international destinations with 7.3% and 5.1% decreases respectively. U.S. carriers reduced capacity again in 2014, partly as a result of consolidation in the U.S., American Airlines eliminated its service to Ottawa as it faced a shortage of pilots for the smaller aircraft serving markets like Ottawa. In contrast, WestJet and Porter domestic volumes for Ottawa increased strongly in 2014.

REVENUES

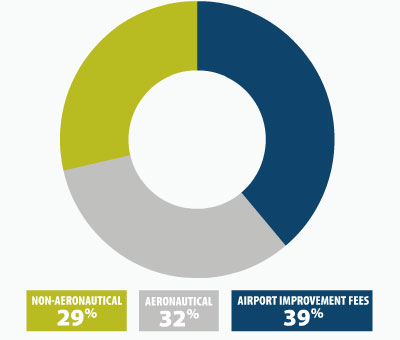

Total revenues increased by 7.8% to $112.3 million in 2014 compared to $104.1 million in 2013.

Airport improvement fees (AIF) at $43.6 million in 2014 increased by 13.7% from $38.4 million in 2013. The increase is commensurate with the increase in the rate from $20 to $23 per enplaned passenger effective March 1, 2014, a ramp up in the collection at this new rate, the passenger volumes in the period, and minor changes in the percentage of departing passengers originating in Ottawa (versus connecting through Ottawa). Passengers connecting through Ottawa are exempt from the airport improvement fee charged by the Authority. An average of approximately 92% of departing passengers originated their flight in Ottawa in 2014 as compared to 91% in 2013. Under an agreement with the airlines, AIF are collected by the airlines in the price of a ticket and are paid to airport authorities on an estimated basis, net of airline collection fees of 6%, on the first of the month following the month of enplanement. Final settlement based on actual passenger volumes occurs at the end of the month following the month of enplanement.

At $36.5 million in 2014, total aeronautical revenues, which include terminal fees, loading bridge charges and landing fees charged to air carriers, were 3.5% higher than revenues of $35.3 million in 2013. The increase reflects a 4.5% increase in landing fee and general terminal fee rates (February 1, 2014) that is offset by the impacts of a 0.8% decrease in seat volumes in the year, and changes in the domestic versus international and transborder mix of flights serving Ottawa. Terminal fee rates for transborder and international flights are higher than rates for domestic flights. As the growth in airline volumes has not kept pace with inflation over the years since transfer, the Authority has again increased its aeronautical fee rates by an average increase of 3.0% effective February 1, 2015. Despite these increases, the Authority’s average aeronautical fee rates remain among the lowest in Canada.

Concession revenues increased by 3.2% from $9.7 million in 2013 to $10.0 million in 2014 as a result of revised concession agreements that eliminated minimum annual guarantees provided under these concession agreements in favour of percentage rents. Through late 2013, the Authority negotiated extensions to certain of its concession agreements beyond their November 2013 expiry resulting in immediate elimination of minimum annual guarantees from these agreements.

Car parking revenues increased to $13.5 million from $12.4 million in 2013, an increase of 8.4%. The increase is commensurate with a change in parking rates on February 1, 2014, and the change in mix of passengers and the availability of parking options. Parking revenues are believed to be most impacted by the mix of passengers. Domestic passengers tend to park for shorter periods of time for business purpose day-trips. Leisure travellers, transborder passengers and international passengers park at the airport for longer periods of time.

Revenues from land and space rentals increased primarily as a result of inflation based adjustments to land lease and exclusive use space rental rates.

EXPENSES

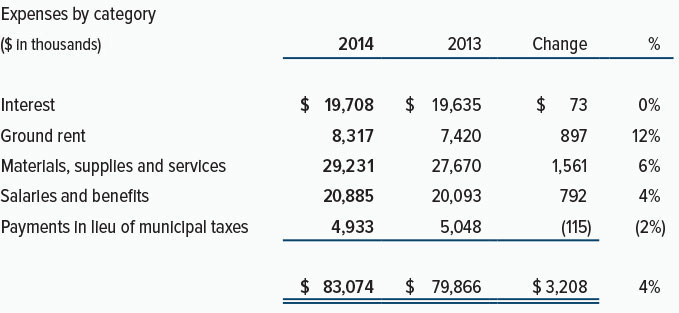

Expenses before depreciation increased to $83.1 million in 2014 from $79.9 million in 2013. Depreciation decreased to $22.5 million in 2014 from $23.0 million in 2013. Depreciation reflects depreciation on continuing investment in property, plant and equipment during 2014, including the Authority’s investment in runway reconstruction in mid-2014. Total depreciation decreased as certain assets became fully depreciated in late 2013 (the 10-year anniversary of opening the terminal building) and have not yet been replaced or needed to be replaced.

Interest expense reflected in the statement of operations results from borrowing to invest in the Authority’s capital programs. Interest expense has fluctuated by minor amounts due to the Authority’s bank borrowing against its credit facilities and repayments of principal on long-term bonds.

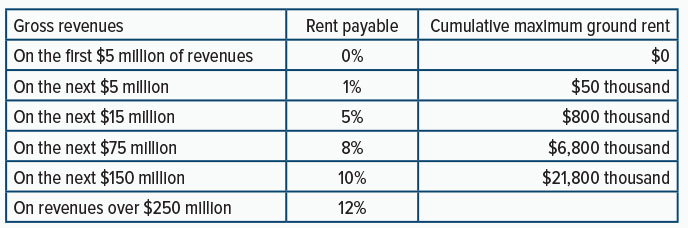

Ground rent payable to the Government of Canada increased by 12.1% to $8.3 million in 2014 due to higher revenues in 2014. The Authority operates the airport under the terms of a ground lease with the Government of Canada that sets out the formula for calculating annual ground rent. The amount reflected as ground rent expense is estimated based on that formula. The formula calculates rent as a royalty based on a percentage of gross annual revenues on a progressive scale. Ground rent is calculated as a percentage of gross annual revenues as defined in the lease, with no rent payable on the Authority’s first $5 million in annual revenue and an increasing rent percentage payable as revenue increases, on a cumulative basis. Rent is levied at a maximum 12% rate on annual revenues in excess of $250 million as follows:

Based on the Authority’s projections, estimated ground rent payments under the ground lease for the next five years are as follows:

The cost of materials, supplies and services increased from $27.7 million in 2013 to $29.2 million in 2014, an increase of 5.6%. In the first quarter of 2014, utilities costs, including electricity, water, and natural gas, all increased significantly. Water costs included retroactive charges for water arising from installation of new meters by the service provider. Most of these additional water charges were charged back to tenants with these chargebacks included in other revenue. The cost of materials, supplies and services also increased due to increased repairs and maintenance costs and contracted rate increases for contracted services, including policing and building cleaning. The Authority reduced the cost of certain of its outsourced services by hiring full time staff to complete these services on a more cost effective basis, but incurred new costs for an outsourced internal audit function, and other professional services. Offsetting these increased costs were lower costs for airfield materials, insurance, repairs to operating equipment, and other items. The winter of 2014 was colder than the winter of 2013, and therefore, the number and duration of winter freezing rain events in the first quarter of 2014 were lower than in 2013. This resulted in costs of airfield materials that were lower in the first quarter of 2014 than in 2013.

The cost of salaries and benefits increased 3.9% from $20.1 million in 2013 to $20.9 million in 2014. Increases resulted from contracted rate increases and an increase in headcount in the Airport Operations Coordination Centre as the Authority replaced outsourced services with employees on a more cost effective basis. These costs were offset by a decrease in the average number of employees charged to regular operations.

The final determination of the Authority’s collective agreement with emergency response personnel, which had expired on June 30, 2011, was settled through binding arbitration in the second half of 2014. The term of the renewed collective agreement for emergency response personnel extended to, and expired on June 30, 2014, coincident with the end of the term for the collective agreement covering the Authority’s other unionized staff. The Authority is in the early stages of collective bargaining for a new contract with emergency response personnel whereas the collective agreement covering the Authority’s other unionized staff was settled in the year with a five-year term that expires on June 30, 2019.

Payments in lieu of municipal taxes have decreased by 2.3% to reflect provincial legislation which dictates the calculation of this payment. Under this legislation, payments in lieu of municipal taxes are based on a fixed legislated rate for the Authority, multiplied by the previous year’s passenger numbers, but to a maximum increase of 5% over the previous year’s amount. The $5.0 million paid for 2014 reflects this prescribed calculation. The number of passengers travelling through the Ottawa Airport in 2013 decreased from 2012 by 2.3%. Payments in lieu of taxes will increase in 2015 by 0.8% from the 2014 amount based on this legislation reflecting the increase in passenger volumes that occurred in 2014.

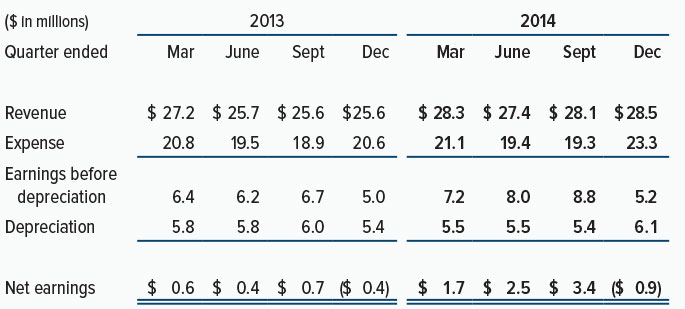

SUMMARY OF QUARTERLY RESULTS

The Authority’s quarterly results are influenced by passenger activity, aircraft movements, maintenance project decisions, and other factors such as weather conditions and economic conditions and do not necessarily fluctuate consistently over time based on the season. Due to these external factors, the historic results on a quarterly basis cannot be relied upon as a predictor of future trends.

Selected unaudited quarterly financial information for the eight most recently completed quarters is set out below:

CAPITAL EXPENDITURES

In accordance with the Authority’s mandate, all earnings are retained and reinvested in airport operations and development, including investment in property, plant, and equipment to meet ongoing operating requirements.

During 2014, the Authority made gross cash payments of $65.3 million related to its capital expenditure programs, and recorded $12.2 million as receivable (of which $11.7 million was received) from the Canadian Air Transportation Security Authority (CATSA) for CATSA’s share in the cost of the airport’s new baggage handling system. Before subtracting this amount from CATSA, the Authority spent over $22 million in 2014 on a project to renovate and expand the airport’s baggage handling system to comply with new regulations for baggage screening. The Authority commenced this project in 2012 and the work will not be complete until late 2015. The total cost of this project and associated work, net of costs to be covered by CATSA, is expected to be approximately $37 million. In addition, in 2014, the Authority reconstructed the airport’s longest runway, Runway 14/32, at a cost of $30 million.

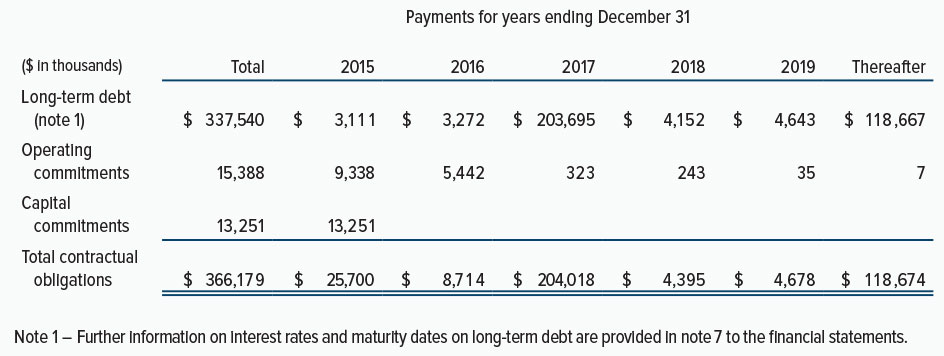

CONTRACTUAL OBLIGATIONS

In addition to ground rent payments noted above, the Authority has operating commitments in the ordinary course of business requiring payments which diminish as contracts expire as follows:

LIQUIDITY and CAPITAL RESOURCES

As a non-share capital corporation, the Authority funds its operating requirements, including debt service, through operating revenues and AIF revenue. The Authority manages its operations to ensure that AIF revenue is not used to fund regular ongoing expenses of operations or sustaining capital. AIF revenue is used to fund debt service costs and other expenses related to the Authority’s major infrastructure construction programs, including the Airport Expansion Program (AEP). The Authority finances major infrastructure expenditures by borrowing in the capital markets and by using bank credit.

The Authority maintains access to an aggregate of $118 million in committed 364-day revolving credit facilities with two Canadian banks. The current facilities have again been extended for another 364-day term expiring on October 16, 2015. Included in such facilities are a $20 million operating credit to fund day to day financial requirements and an additional $98 million in the aggregate to fund general corporate purposes, to provide liquidity support, and to fund major capital expenditures on a short term basis prior to securing longer term financing in the capital markets. After subtracting draws against these credit facilities of approximately $49 million as at December 31, 2014, the Authority has approximately $69 million in available unused liquidity, of which approximately $12 million has been allocated exclusively to an Operating and Maintenance Reserve Fund. The Authority believes that this available unused liquidity is adequate to meet its future plans and requirements.

In 2002, during Phase I of the AEP, the Authority established a Capital Markets Platform under a Master Trust Indenture (MTI) setting out the terms of all debt, including bank facilities and revenue bonds. Under the MTI, the Authority is required to maintain with the Trustee a Debt Service Reserve Fund equal to six months’ debt service. At January 27, 2015, the balance in the Debt Service Reserve Fund was increased to $11.1 million, which exceeds the amount required under the MTI. The MTI also requires that the Authority maintain an Operating and Maintenance Reserve Fund in an amount equal to 25% of defined operating and maintenance expenses for the previous year. This fund may be maintained in the form of cash and investments held by the Authority, or the undrawn availability of a committed credit facility. As at December 31, 2014, $12.0 million of the Authority’s credit facilities had been allocated exclusively to the Operating and Maintenance Reserve Fund. At December 31, 2014, the Authority was in full compliance with the provisions of its debt facilities, including the MTI’s provisions related to reserve funds, the flow of funds and the rate covenant.

The Authority has accessed its existing bank credit facilities to fund the costs related to its capital expenditure programs and expects to access these facilities on an ongoing basis to fund these programs. The Authority completed 2014 with bank indebtedness of $48.7 million as a result of investing in its capital programs. Based on its current plans, the Authority’s maximum borrowing requirements under these facilities is not expected to exceed $68 million during 2015. From time to time, surplus cash is invested in short-term investments permitted by the MTI, while maintaining liquidity for purposes of investing in the Authority’s capital programs.

The Authority’s accounts receivable increased by $3.5 million during the year as the result of the increase in AIF from $20 to $23, an increase in HST input tax credits resulting from the Authority’s capital expenditure programs, and an amount receivable from CATSA of $0.5 million related to the baggage handling system costs. The post-employment benefit liability decreased by $2.5 million in the year. The change in this liability resulted from a number of offsetting factors. Pension solvency payments made during the period of $2.5 million, and investment returns in the year that were in excess of the 2013 year end discount rate of 4.75%, were offset by the impact of re-measuring the liabilities at a 2014 year end discount rate of 4.0%. $0.9 million has been recorded as other comprehensive income in the statement of operations and comprehensive income to reflect investment gains net of liability re-measurements.

During 2014 and early 2015, Standard & Poors and DBRS reaffirmed the Authority’s credit ratings with stable outlooks in respect of the Authority’s revenue bonds under the MTI at A+ and A(high) respectively. Moody’s reaffirmed the Authority’s credit rating with a negative outlook at Aa3.

RISKS AND UNCERTAINTIES

LEVELS OF AVIATION ACTIVITY

The Authority will continue to face certain risks beyond its control which may or may not have a significant impact on its financial condition. Airport revenue is largely a function of passenger volumes. Passenger volumes are driven by air travel demand. The events of the past several years have emphasized the volatile nature of air travel demand and the impact of external factors such as economic conditions, health epidemics, geopolitical unrest (September 11, 2001), government regulation, the price of airfares, additional taxes on airline tickets and the financial uncertainty of the airline industry.

The financial uncertainty of the airline industry, although currently relatively stable in Canada, remains an ongoing risk to the Authority. This is mitigated by the fact that approximately 92% of the passenger activity at the airport originates or terminates at the Ottawa Airport, as opposed to connecting through Ottawa. Connecting passenger volumes are more vulnerable to fluctuation due to routing and scheduling changes by airlines. In addition, a greater percentage of the traffic through the airport is business travellers, whose travel decisions are less discretionary than those of leisure travellers.

AVIATION LIABILITY INSURANCE

The availability of adequate insurance coverage is subject to the conditions of the overall insurance market and the Authority’s claims and performance record. The Authority participates with an insurance buying group that also includes airport authorities from Vancouver, Edmonton, Calgary, Winnipeg, Montreal, and Halifax. This group has been successful in placing all of its insurance needs. In previous years, there have been significant changes in the insurance markets for aviation, largely driven by the events of September 11, 2001. These events limited certain insurance products and resulted in higher pricing. The Government of Canada has extended an indemnification for third-party aviation war risk liability for all essential aviation service operators in Canada. The Government of Canada has indemnified the Authority for losses in excess of U.S. $50 million, the limit of insurance coverage which is currently available to airport operators on the market. The Government of Canada originally provided this indemnification in response to a decision by international insurers to withdraw third-party aviation war risk liability coverage that was available before September 11, 2001. The Government of Canada has given no indication that it will cease providing excess indemnity coverage.

Total revenues increased by 7.8% to $112.3 million in 2014 compared to $104.1 million in 2013

2014 Revenues

SUMMARY OF AMOUNTS SPENT IN THE OTTAWA REGION

PASSENGER GROWTH BY SECTOR

Five-Year Review

Five-Year Forecast

AIRCRAFT MOVEMENTS

TOTAL NONSTOP DESTINATIONS

DAILY NONSTOP FLIGHTS

ORIGIN AND DESTINATION

SUMMARY OF AMOUNTS SPENT IN THE OTTAWA REGION

PASSENGER GROWTH BY SECTOR

Five-Year Review

Five-Year Forecast

AIRCRAFT MOVEMENTS

TOTAL NONSTOP DESTINATIONS

DAILY NONSTOP FLIGHTS

ORIGIN AND DESTINATION